Citigroup’s 25-Year Chart before next week’s Earnings Report

Photo: Huffington Post

Selerity Global Insight– Citigroup (C) is scheduled to report 4Q 2016 earnings before the opening bell on Wednesday, January 18th. The results are expected to come through at approximately 8:00 a.m. ET with a conference call webcast at Citigroup Investor Relations to follow at 11:00 a.m. Citigroup has the potential to impact the broader market indices, including the S&P Index Futures and corresponding ETFs. The earnings release comes after most of the other money center banks.

Outliers & Strategy

Key measures:

- Adjusted Earnings Per Share (EPS): Analyst consensus is $1.12 (range $1.07 to $1.18). (Source: Yahoo! Finance) Consensus was $1.19 three months ago.

- Revenues: Analyst consensus expectations are for a 7.1% y/y decline to $17.32 bln ($16.91 bln to $18.24 bln).

- Citigroup shares have a Price/Book of 0.8 compared to the 5-year average of 0.7. The stock trades at 13.0x trailing earnings vs a 5-year average of 13.8x. Price/Revenue of 2.5 compares to a 5-year average of 1.9. Price/Cash Flow of 6.6 compares to a 5-year average of 4.9. A dividend yield of 0.7% compares to a 5-year average of 0.3%.

- Analysts view Citi with 15 Buy, 8 Hold, and 2 Sell ratings (source: MarketBeat.com).

- Insiders sold a net 953,237 shares over the last three months and a net 268,400 shares in the past year (source: NASDAQ.com). Citigroup will increase its common stock repurchase program to $8.6 billion when the current $7.8 billion program ends in Q3. The new program will expire at the end of Q3 2017.

- Citigroup shares have a 1-day average price change on earnings of 2.57%. Options are pricing in an implied move of 2.71% off earnings.

Recent News

- 01/03: Barclays named Citigroup among as a bank with an Overweight rating for 2017 citing potential for higher interest rates/steeper yield curve; lower tax rates aiding EPS, asset quality, and economic growth. A less cumbersome regulatory environment also should help lift valuations, according to a post on Barron’s.com.

- 12/21: Moody’s believes the Fed’s new TLAC rule won’t affect Citigroup as they already meet the capital requirements to buffer against any potential future losses in a crisis, according to a post on Barron’s.com.

- 12/14: Citigroup would benefit least from a rate hike as its interest rate sensitivity is the lowest among its banking peers, according to a post on marketrealist.com.

- 12/09: Guggenheim Securities sees benefits for Citigroup from the yield curve having steepened sharply following the presidential election. Bank net interest margins (NIMs) should benefit modestly in the fourth quarter with more significant improvement in 2017. Mergers and acquisitions (M&A) volume is up quarter-over-quarter and is on track to be up year-over-year, according to a post on Barron’s.com.

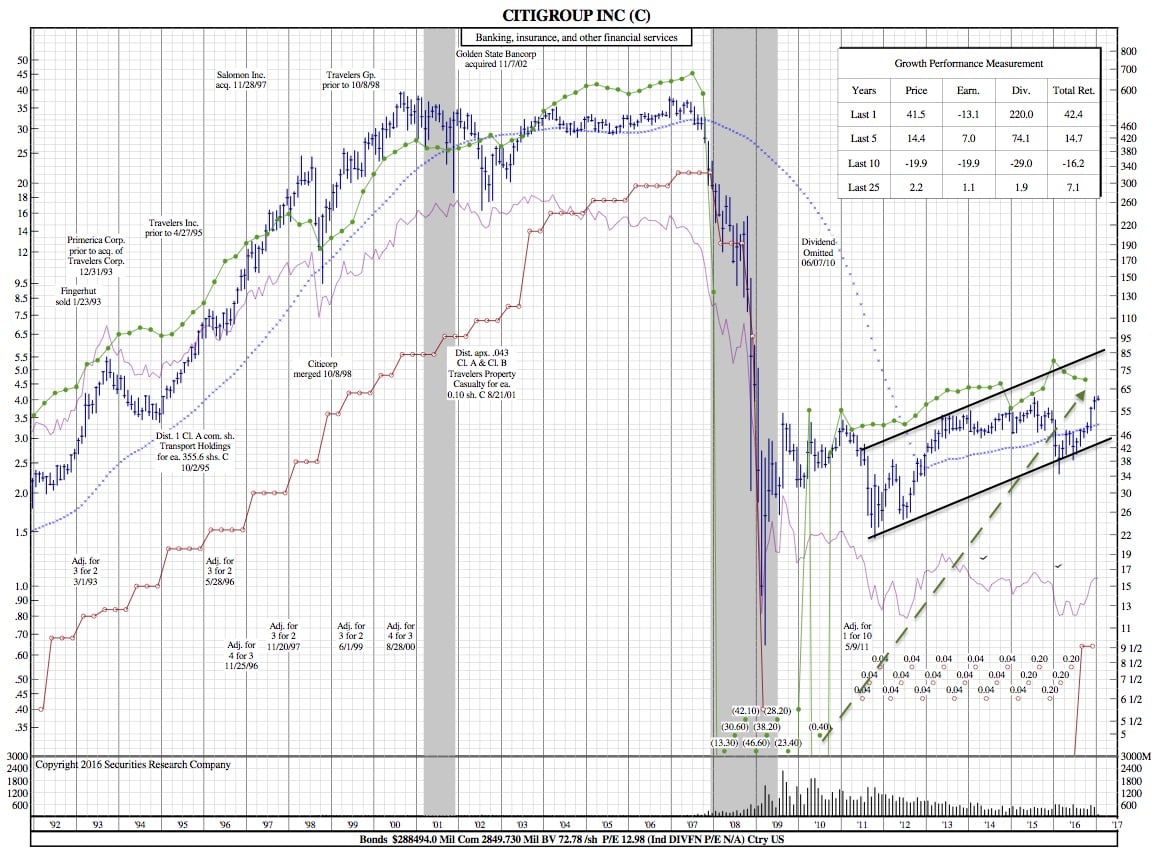

Citigroup 25-Year Chart:

Citi shares underperformed other money center banks since the financial crisis, but shows average performance the past two years. The stock is currently testing the 2015 high. Point and figure technicians have increased their bullish price objective to $105 from $69 but these target increases often have terrible timing.

click to enlarge

Summary

Citigroup shares have disappointed relative to the other big banks for a decade. The increased insider buying over the past year was recently rewarded and they sold nearly a million shares into the recent rally. Citi still has nearly $45 bln in deferred tax assets which can enhance future earnings or add value in the event of a breakup. Citigroup has beaten analyst consensus by an average of 8c. Estimize consensus for Adjusted EPS of $1.13 on revenue of $17.271 bln compares to analyst consensus of $1.12 on revenue of $17.32 bln.